A man is not a plan

The challenges of empowering women to become financially independent

The world has never been an equal place for men and women in terms of social standards, rights and economic opportunities. Even now, as technological development reaches the point where space tourism seems like the next step for humankind, women are still fighting for the same opportunities that males have had for centuries. Yet, it is often argued that much progress has been achieved in the last century and that the majority of women on the planet already have the right to study, work and vote. Is it the truth? Are we close to equality?

Many global research institutes have been trying to assess the existing gender gap in the world by various dimensions like education, labor force participation, financial and economic participation, political rights, healthcare indicators among others. For example, the World Economic Forum (WEF), in its Global Gender Gap Report 2020, stated that gender parity will not be attained for another 99.5 years, meaning that it will definitely not happen in the lifetime of current adults and teenagers unless urgent and drastic measures are applied. The report argues that no country so far has achieved full gender parity. Among the four subindexes, “Political empowerment†and “Economic participation and opportunity†have the highest global gender gaps that need to be closed, at 75% and 42% respectively. The two remaining ones, “Educational attainment†and “Health and survival†have significantly smaller gender gaps – 4% and 3% respectively.

What do these numbers say about the position of women in the world? The most evident fact is that women remain far behind in terms of economic participation. This is because they are often dependent on men – in fact, a woman’s standard of life worldwide generally depends on that of a man, be it their father, husband, or partner. Financial independence still remains one of the most significant challenges for women around the world to overcome.

The belief that a man will always provide financial security is one of the most crucial illusions, or traps, that prevents women from gaining their financial independence or improving their current financial condition. When a woman financially relies on a spouse or partner, she puts herself in a more vulnerable position than she was before the marriage or relationship.

Women remain financially vulnerable even in those cases where they are educated, have a full-time job, good career prospects and are in an official relationship with a supportive and non-abusive spouse or partner:

- Women earn less. According to the WEF’s 2020 report, only about 55% of women in the world are in the labor market. Furthermore, even these working women earn only 40% of the wages and 50% of the total income of men.

- Women tend to choose occupations that are lower paid. Reasons for this vary across different countries, but include cultural norms and “glass ceilings.†Sometimes it is a women’s choice to take positions with less responsibility, but sometimes they have no other option.

- Education does not always help women get a well-paid job. This is the main reason why educational attainment does not seem to directly affect economic participation: for instance, according to WEF’s 2020 report, global “Educational attainment†is set to reach gender parity in 4 years, while “Economic participation and opportunity†will take 42 years.

- Maternity leave contributes to a reduction in working years, which directly affects their retirement savings and, as a result, their quality of life in old age.

- Women live longer. According to World Bank data for 2018, the global average for male life expectancy at birth was 70.4 years compared to 74.9 years for women. In many countries, the difference in life expectancy was significantly larger. This means that women rely on their pension savings longer, while these retirement savings are smaller because, on average, they have lower-paid occupations and more career gaps due to maternity leave. With the average global mortality rate of adult males being significantly higher than the rate for women, married women face a higher probability of being left alone.

- The rates of divorce and births outside of marriage have been increasing across the world, meaning that women face a higher likelihood of having to provide for themselves and their children alone. The situation is worse in developing countries, because of corrupt and inadequate legislative and judicial systems that permit men to evade paying alimony or not paying a fair amount.

- Women often face physical and psychological abuse. In 2015, the World Health Organization (WHO) reported that 1 in 3 (around 35%) of women worldwide experience physical and/or sexual intimate partner violence or non-partner sexual violence in their lifetime. Moreover, the WHO in 2020 also reported that over 15% of elderly people over the age of 60 in Europe were affected by various types of abuse in 2019, meaning that elderly women are in an even more dangerous position than younger women.

Some experts propose financial literacy and financial education programs as solutions that can empower women and overcome the challenges of financial dependency. However, some research suggests these programs may not be effective, primarily for the reason that financial education cannot guarantee a change in attitudes or behavior.

Whether education programs are effective or not, we do know what concrete steps every woman in the world can follow to strengthen her position, as long as she has a job or cash income from any source. The actions become more complex the further you go down the list – a woman can start from the step that she feels comfortable with.

10 steps to building financial independence

- Calculate a personal “financial airbag†for a period of at least six months. This will be the sum that will cover the necessities for a woman and her children in a specific period. The airbag will help her to feel comfortable in case of a loss of the main source of income (job, spouse support).

- Set a goal of saving a specific amount. The initial goal can be to gather the financial airbag, but it should be increased if the circumstances permit. Having a solid calculated target will serve as the main motivation, rather than just saving for the sake of saving. It is also beneficial to have an emergency fund ready for any event.

- Spend less than is being earned. A basic rule, but many struggle with following it. A woman should save 10%-30% of her monthly salary (or other income), preferably in a savings deposit account.

- Create a financial plan – both short-term and long-term. What are the savings for? Education? New business opportunities? Better retirement conditions? The plan has to have milestones in it with concrete numbers. It will change along the way, but it will help with navigating any future life paths.

- Make wise investments. Multiply your savings. A woman can start with a deposit account, but after years or even decades, her savings might be enough to invest in different financial instruments or real estate. In other words, during the process of saving a person should learn how to invest and where to invest, because one day they may be able to do it.

- Diversify investments and sources of savings. The golden rule — never put all your eggs in one basket. Women have to learn about and explore the different financial options available.

- Seek professional financial guidance. When a woman accumulates enough financial resources and starts investing them, additional competence will be a great help in this process. It can be in the form of specific financial courses or enlisting a personal financial advisor.

- Seek career development. A woman should take every opportunity to move up in her role and education level. With enough money in her bank, she can look for a better and more highly paid job or receive a new degree without fear of financial instability.

- Network to find your support system. Although a research study confirmed that female professional networks are less powerful and effective in terms of exchange benefits and motivation than male ones, networking is important; it creates new educational and job opportunities and it helps when a person is in a financial crisis. It can be the greatest lifelong tool for improving women’s financial status.

- Discuss financial safety with your spouse or partner. This last step can and should be implemented at any step of the way and should be done multiple times over your lifetime. The topic of financial safety should be brought up when family circumstances changes – giving birth to a child, a woman’s decision to stay a certain period of time on maternity leave, change of city or job, a national or international financial crisis affecting jobs or salaries of family members, or any other life-altering event. Both spouses need to make sure that they have financial safety options in any situation.

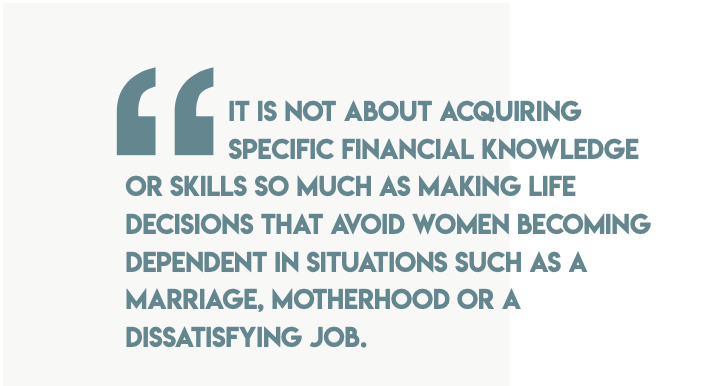

This list of steps might seem like a strategy; but is better conceived of as a concept of living. It is not about acquiring specific financial knowledge or skills so much as making life decisions that avoid women becoming dependent in situations such as a marriage, motherhood or a dissatisfying job.

Financial independence matters for every woman – from single moms and married housewives to women working full time or part-time with high or low salaries. Today, it is vital to have a financial plan for life and to control and monitor your financial status. A woman not only has to be financially literate but, more importantly, she needs to bring knowledge to this practice. It is also important to be financially included – to have access to the services of financial institutions. All these skills and activities can be summed up by one simple recommendation – women everywhere have to be proactive in their financial lives and rely on themselves to become financially independent.

Want to read more inspiring stories about women in leadership?

Download the Geneva Business School Magazine now.

The views expressed in this magazine are those of the authors or interviewees and do not necessarily reflect the opinions of Geneva Business School or the editors of the magazine.